by Ameya Paranjape –

The economic impact of the COVID – 19 pandemic highlights the need for the 6,799 FDIC insured banks to become more agile and modernize the banking infrastructure to be able to quickly react to changing economic conditions. When the United States Federal government announced the Payroll Protection Plan (PPP) through the Small Business Administration (SBA) we noticed the larger banks were struggling with being able to respond while the mid-tier and regional banks had an unprecedented opportunity to acquire new customers. The banks that had invested in cloud-based solutions were even better positioned to acquire a lion share of the new opportunity.

Traditional Banking Core Systems

Before we talk about becoming a nimbler organization, we must understand the current state of the banking core systems.

The majority of mid-tier and community, regional banks are using a bank-in-a-box architecture in which all core deposit, lending, and customer operations are all handled by the same mainframe system. This places an undue burden upon banking operations as they must use the one size fits all solution and therefore lack the flexibility to meet specific business opportunities as they arise.

Transform to Flexible Niche Solutions

The future trends are showing the focus is on the increased usage of niche competency, best-in-breed, point solutions from the ever-increasing number of Fin-Tech companies. This focus allows banking operations to focus on solutions specific to each area’s requirements instead of an inflexible monolithic solution. These solutions allow the business to pivot and respond rapidly to meet the economic environment in days and not months.

Mining the Data

When technology historian’s look back at this time, they will remark on the trend of the data revolution. Every company has mountains of data, but companies are just now starting to leverage the insights locked away in their data marts and lakes. We are seeing a trend of transformation from basic reporting of financial information to predictive models, consumer behavior forecasts, and personalization solutions that meet the customer on their terms. All of this is coming into rapid focus as millennials continue to enter the workforce and marketplaces. Consumer behavior has changed and the tools we use to serve our customers are changing as well.

While the data that companies contain within their firewalls can be considered the new gold, it can quickly become stale. Statistically, over the last decade, we’ve seen an immense increase in the amount of effort needed for every organization to tap into multiple data sources and harmonize the data into usable formats. By the time that’s achieved, the shelf-life or usability threshold of that dataset is reduced to less than a week and in some cases to just one day.

Harnessing the Cloud

The cloud provides a paradigm which enables banking operations to utilize best-in-breed products for specific lines of business and use cases. Building a cloud backbone through microservices allows systems to operate independently, refer to a common set of data elements, offload work to a system dedicated to the task, and scale on demand.

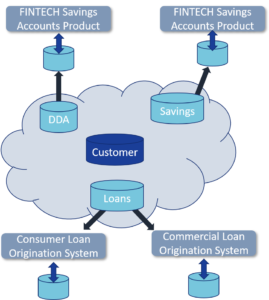

Sample cloud infrastructure

Distributed Architecture

Banking operations can decouple the monolithic bank-in-a-box into focused systems, thereby dynamically meeting the specific business need. Each business area can use a system focused on their specific needs and business opportunities while IT meets the operational need with a combined view of the data. Each supporting system will have ties back into the cloud referring to data, business rules, and reporting needs but still can operate independently.

Agility

Through the cloud microservices, new applications and functionality can be operationalized in days instead of weeks or months. Because the cloud has previously in-built functionality, it provides the ability to focus on tasks such as developing a new front end and making business rules or other operational efficiencies but not tasks that require a focus on back end processing.

Data Reusability

Historical transaction data and application data can be used for multiple cross relational initiatives. Once a subsystem has cleansed the customer data, that data can now be used by any application in the enterprise with a high degree of accuracy.

Data Centralization

Using the hub and spoke method, the cloud will enable a common set of data elements and terms for all systems to read, use, and update. This reduces the need for multiple data marts, data lakes, and other data storage for each subsystem and creates a single repository for common analytics and data redundancy.

Scalability

The cloud can expand upon demand reducing the need for a big bang approach.

For example, data from the mainframe can be moved to the cloud and then methodically separated for each relevant system limiting disruption to the business. As the business demand grows and spikes, the cloud can respond accordingly.

Cost-Effectiveness

Cloud providers have many different options for computing usage that can be used when employing the cloud. When choosing the various options, it is critical to be aware of the business case for computing needs. For example, it is far cheaper to put a customer’s historical data into cold storage and leave the current month or two in high-speed data storage.

Artificial Intelligence (AI)

With all data in one location, standardized, and with access to significant computing power, banks are now able to apply data analytics and artificial intelligence to gain insights into customer behavior and trends.

Optimizing the Bank, Reducing Costs, and Improving Customer Service

Branch Transformation

The concept of a brick and mortar building is slowly becoming defunct as more bank customers are using web and mobile applications. Some financial organizations such as American Express have gone completely virtual, but that business model does not work for the smaller, regional banks who must have a local presence due to their customer demographics. This forces the bank operations to understand the viability and feasibility of keeping a particular branch location open or the location of the next branch and determine the staffing needs.

Using third-party data such as real estate analytics, census data, local area demographics, competitor branches, and other relevant data aggregated with a bank’s existing customer data such as the number of transactions and bank account holder address, predictive analytics models can be created to optimize the bank location and staffing patterns.

Results of branch transformation include higher customer satisfaction as well as reduced resource and infrastructure costs.

Loan Operation Optimization

Lending operations are provisioned through specialized loan origination systems that follow a complex and intricate process with many data points acquired from the customers. They include validation of facts, acquiring best interest rates, managing, and servicing the loan components that encompass risk assessments, loan review, and other analyses.

The cloud infrastructure provides capabilities to simplify and optimize the loan process. For example, the PPP loans were announced, and banks were required to quickly gather data, underwrite, and fund the loans with limited guidance but with the ability to expand the bank’s account base at the same time. Banks with appropriate cloud solutions were able to respond quickly due to significant process automation:

- Application Process: Provide a front end to capture the data elements as required by the loan application process

- Document gathering: Use existing secured document collection to tie the records to the application

- Business Rules: Set up business rules for automated evaluation of the loan for immediate response to the customer of denied or sent for review

- AI: Use AI/Robotic Processing Automation to review the supporting documents, extract data and update the loan application system

- Data Analytics: Blend customer application data with existing bank records to assign applications to various work queues based on business rules

- Loan application: Update loan servicing tool for the new product and use built-in triggers to automate next steps

- DocuSign: Provide loan documents for signature

- Reporting: Use real-time dashboards to manage portfolio and track funding processes

Loan operation optimization improves many areas, resulting in faster time to market and cost savings due to automation efficiencies.

Customer Analytics

Cloud operations provide banks advantages from cutting-edge data analytic tools and techniques that are impossible to implement in a traditional, legacy environments. Instead of building data marts or exporting data, banks can purchase analytic software with in-built features for reviewing customer data and identifying trends for marketing and adjustment of business practices.

For example, fee analysis is very important for retaining customer loyalty. If a customer is a heavy user of banking services, the bank can waive fees for a high-value customer based on predefined business rules backed by data science analysis. The decision to waive a fee can be built into the data analysis module of the existing platforms-as-a-service thus externalizing the process and providing consistency in waving fees.

Customer analytics results in increased customer awareness, increased customer activity and revenue, and better investment decisions regarding high-value customers.

Achieve Measurable Business Outcomes

The migration from the trusted and known legacy applications to a cloud-based architecture can be challenging. Using a slow and easily digestible approach to cloud migration iteratively modernizing smaller pieces of the overall system can achieve measurable results such as significant cost savings, increased revenue, and faster time to market with predictable delivery.

Regardless of the cloud platform solution chosen, the key is to build cloud-native services with a robust, scalable, optimal architecture that can easily adapt to the ever-changing technology landscape through the plug and play distributed paradigm.

For the journey to the cloud to be a success, you need a trusted partner like RCG with deep domain knowledge in the leading cloud platform solutions and experience with the retail banking industry. We can bring not only platform expertise to the journey but also in-depth business knowledge and subject matter expertise to analyze, build, and accelerate the development cycle of any cloud program.