by Joe Mendel –

“Happiness is stopping to smell the cookies” – said everybody ever

Experiences are what make life memorable and provides levels of trust, comfort, and happiness.

Psychologist Nicole Celestine tells us, “In general, happiness is understood as the positive emotions we have in regards to the pleasurable activities we take part in through our daily lives.

Pleasure, comfort, gratitude, hope, and inspiration are examples of positive emotions that increase our happiness and move us to flourish. In scientific literature, happiness is referred to as hedonia (Ryan & Deci, 2001), the presence of positive emotions and the absence of negative emotions.

Our brains come already designed for happiness. We have caregiving systems in place for eye contact, touch, and vocalizations to let others know we are trustworthy and secure.”1

Let me give you some examples. If we were in a conference room, I would ask you to close your eyes while I painted a verbal landscape for you, but the following examples should provoke some emotion.

Making your way in the world today takes everything you have got.

Throughout the 80’s and into the early 1990’s there was an immensely popular classic television program called “Cheers”. It was a situational comedy set in a bar called “Cheers” where friends gathered regularly to interact and to share experiences. The characters evolved into an extended social family, and everyone knew everyone else’s quirks and idiosyncrasies. Even the theme song called it a place where you went because it is where “everyone knows your name”. For example, one character, Norm, played by Chicago native and former Second City performer, George Wendt, would come through the door and everyone in the bar would welcome him by verbalizing “Norm” as he came down the steps and to his normal seat at the bar where, because he came in everyday at the same time, his drink of choice would be waiting for him, and the banter would begin.

Or let me give you another experiential example that may hit much closer to home. We all have a favorite relative, whether it is your grandmother, mother, sister, cousin, whatever whom you delight over visiting because you know when you walk through the door, you can smell your favorite coffee or tea brewing and you know that your olfactory senses are also picking up the hint of the hot freshly baked molasses cookies that you loved as a kid – which you know are just coming out of the oven and will soon be on the plate for you as soon as you sit down.

So, what do the two examples have in common? It is emotional attachment and the happy feeling that “someone” knows you and knows what you like, what is important and most crucial, what is relevant.

Financial institutions for years have been talking about getting to a point where they have attained the summit of a 360-degree view of the customer only to, like the mythical Sisyphus2, have the rock roll back down on them (the eternal punishment) as ever-increasing amounts of data are available to them from new sources.

Historically financial institutions sat on a tremendous cache of information about the behaviors of their client base. From their interactions they knew, where clients lived, the family makeup, if they owned their home, had a car (or two), a boat, college aged children. They knew if they had a savings account (maybe a special purpose like a Christmas club or vacation account), and a checking account and from the activity, knew where they wrote checks for groceries (or used the debit card), what utilities they paid, what internet, streaming services they used; whether they used the branch or banked online, or mobile or ATM (time of day and locations); where they worked because of payroll deposits; if you shopped online at Amazon, what you bought, time of day they bought and method of payment on what device, etc. I could go on and on. These are all data points that early on were unorganized and uncategorized and just random bits of information. Later they were all collected in data warehouse designed to hold the data for manipulation in getting to that 360-degree view. Bankers are still trying to tie all of the systems together to do this but that is for another blog.

So let us fast forward to today, where this is just table stakes (there is some degree of the 360 view) and banks now advanced analytics help them understand how to monetize the value of the data points and the particular behavioral aspects of a client to create a more contextual view of customer journeys, attributes and needs. But here again, data points alone do not make an emotional connection that would cause a positive reaction with the customer base that molasses cookies do. This is where the gap exists. And this is where the evolution of the interaction with customers needs to go to create competitive advantages, corporate sustainment and increased profits from lifetime value and wallet share (and maybe, more accurately, MIND share).

Rock ‘n Roll Again

Emotional connection comes from putting that human aspect in place by learning from historical interactions (existing data points) in order to optimize future interactions (contextual and relevant predictive and prescriptive offerings), with a unique customer (journeys and personas) creating outcomes (increased mind share, lifetime value, retention), financial health and well being of the client population (guidance and financial literacy) that lead to emotional connection and competitive advantage. All of which are characteristics of more intelligent customer interactions and experiences.

Well, now let us take the linear progression from collection to housing to manipulation then distribution of data assets and complicate it even more, but at the same time tee us up for a step closer to true intelligent customer experiences.

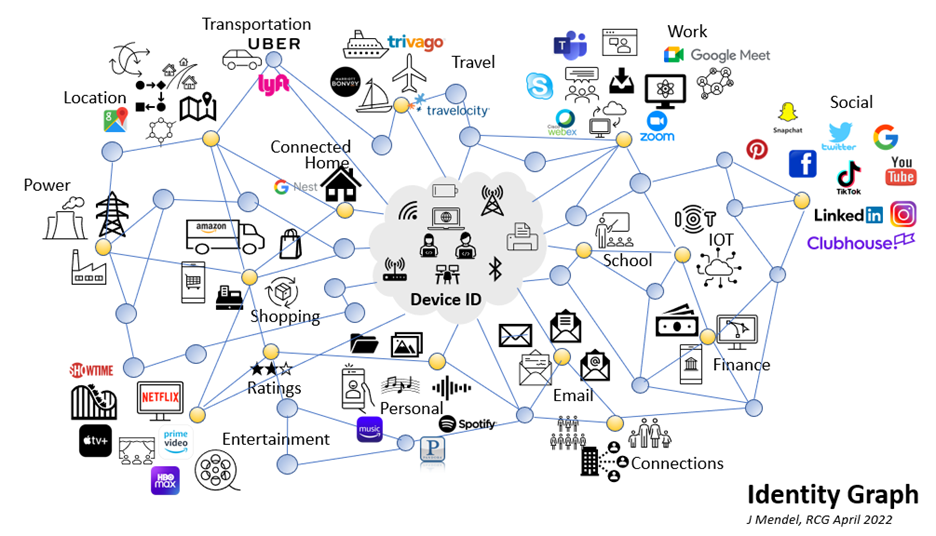

Cisco tells us that it estimates that currently there are 5 QUINTILLION bytes (equivalent to a billion gigabytes or five exabytes) of information generated each day from wearables, smart home devices, smart industries, smart cities, combining AI, 5G and big data to create a smart connected network the AIoT. Add this to alternative sources of information from social media interactions, and the rock begins to slide back down the hill again. The front end of information gathering begins to create an identify graph like this:

The point is that there are already millions of additional behavioral data points available in near real time via a huge 5G pipe (and very soon 6G). Financial service organizations that do not plan today to architect their intelligent customer service structure (yes, I am proposing this as an internal operating model) to leverage are doomed to push the rock again. Time-to-market with an intimate understanding of emotional connection is the new playing field. Think about IoT sensors embedded in roof shingles that alert customer that it is time to replace and a bank already ready to approve a home improvement loan. Or a furnace or air conditioning unit with sensors indicating that it is failing or an exhaust system on a car needing major repair/replacement. This is predictive intelligence and intelligent experience in practice through the leveraged use of new data sources.

RCG Global Services in its recently released e-book entitled, “Drive Customer Experience with Purposeful Digital Enablement” describes how to harness this power of data and get ahead of the Sisyphus paradox. It states, “Investing in improved customer engagement simultaneously accomplishes three important objectives: it increases the lifetime value of existing customers, it enhances the quality of customer experiences and customer satisfaction, and it ultimately results in greater business growth.”

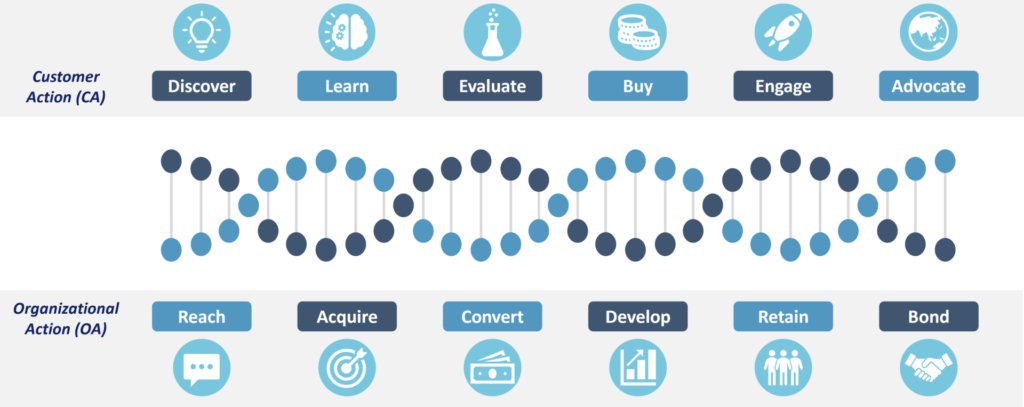

When the emotional needs of the customer are attached to the behavioral data it results in a unique intelligent customer experience that is illustrated by a framework and platform called CxDNA. CxDNA organizes your decision-making process into two interwoven strands of component “molecules” for intelligent interaction along the intelligent customer journey.

This results in the creation of the emotional bond that is foundational to the intelligent customer experience as we have seen.

Sweet smell of connection

Financial service organizations are approaching the apex of the hill with respect be being able to function as technology marketing companies that offer financial products that make a real emotional connection. The next step is to harness data and monetize it to be able to sell with the intimacy of Google, Amazon and Facebook but with the experiential intelligence of the trust and security of being in that place “where everybody knows your name, and they’re always glad you came” and of course, that has those molasses cookies.

Takeaways

- Lay the groundwork for capturing new sources of alternative data available within the AioT metaverse to supplement traditional existing data points,

- Utilize cloud-based warehouses and real-time transport mechanisms to deliver meaningful data to create competitive speed-to-market velocities,

- Incorporate Artificial Intelligence, Machine Learning and other technologies like Natural Language Processing to connect the dots and make inferences that are relevant to the personas,

- Take advantage of 5G, Wifi6 and Web3 advances to augment data capture and real time deliveries,

- Finally, leverage all the technologies to support a human-hybrid model that relies on digital assistants and bots to deliver information needed into the hands of humans allowing them to interact with customers and create that emotional “experiential” bond that is the heart, the CxDNA, of the intelligent customer experience.

We at RCG Global Services are available to help you drive your digital revolution through our solutions, practices and advisory services. We help Financial Service organizations understand the complexity of remaining viable and competitive in todays on-demand ever-evolving consumer economy. We have been successfully solving complex business problems for financial service companies globally since 1974. Our clients rely on us to help them harness the speed of now that drives evolution to the hyper-business age. We know companies struggle to exist in an ecosystem of three simultaneously co-existing strategic states, where the adoption of an evolutionary mitosis process constantly transforms and evolves operational and engagement models. Our engagement model has evolved also to provide the expertise necessary to identify evolutionary solutions and get you from mode-to-mode efficiently with minimal disruption, allowing you to off-load, and de-risk your most critical strategic and competitive initiatives.

We ask questions to solve business problems. We engineer the velocity necessary to create competitive advantage through impactful outcomes. We make your strategy a reality by compressing the time between strategy on paper, to execution, to impact, maximizing returns on investment while creating competitive advantage.

“We prepare you today, to meet the speed of now, needed tomorrow.”

Works Cited

1. The Science of Happiness in Positive Psychology 101, PositivePsychology.com, Nicole Celestine, Ph.D., 28-03-2022

2. Zeus, fed up with Sisyphus’ tricks and cunning as well as his hubris – believing he was more cunning than Zeus – punished him to eternally push a boulder uphill. However, as soon as he would reach the top of the hill, the boulder would roll off and Sisyphus had to push it back again. Source: https://www.greekmythology.com/Myths/Mortals/Sisyphus/sisyphus.html