Every year, the fantastic folks at Cornerstone Advisors produce their “What’s Going On In Banking” report. The report aims to summarize an extensive executive survey conducted across community banks and credit unions.

In 2021, the reports author Ron Shevlin wrote “Digital account opening (DAO) stays hot. For the fourth straight year, digital account opening is at the technology for which banks and credit unions will select a new or replacement system. It’s also at the top of the list of bank/fintech partnerships. Hopefully this will be the last year financial institutions obsess over DAO and start focusing on other capabilities they’ve been ignoring.”

In 2022, Ron wrote “Digital account opening systems are still hot. For the past four or five years, digital account opening systems have been at the top of financial institutions’ list of planned new selections/replacements. What’s taking the industry so long to get this done?”

And in this year’s report for 2023… “Expectations among credit unions to select a new consumer digital account opening platform is high for 2023, as it was going into 2022. But in 2022, only about half of the percentage of credit unions that anticipated making a new selection actually did so.”

What’s the problem?

As someone that’s been involved in Digital Account Opening (DAO) for over a decade – delivering solutions for clients ranging from Citibank and HSBC to community banks and CUs, I thought I’d offer up my thoughts on the challenges I’ve seen.

1. Prioritization (if it ain’t broke, don’t fix it)

Many banks and credit unions have digital account opening, and it’s working ‘fine’. As we all know, when you ask someone how they’re doing and they say ‘fine’, that’s another word for ‘bad’. We’ve seen DAO solutions with 40% – 50% approval rates. Yes, there’s fraud in deposit accounts. But not THAT much. Many institutions have come to accept that 50% approval rates for digital is ok. It isn’t. I’ve worked with institutions with 70% – 80% approval rates on DAO with no elevated instances of fraud or bad accounts.

So my message to institutions struggling to prioritize DAO is “It IS broke, fix it!”.

2. Legacy mindset (people love coming in to our branches)

Some people absolutely love the fact that their bank has a branch. Most people who value the branch do so because it’s somewhere they can go to make a human being accountable for any issues with their money – it’s hard to hold someone on webchat accountable for money missing from your account…never mind a chatbot. But if I go in to a branch and speak to the manager, I’m making them personally accountable and I like being able to do that.

However – when it comes to something transactional like opening a checking or savings account, people value convenience. Institutions that have been successful with their DAO solutions have found that the Digital Channel out performs ALL branches combined when it comes to the origination of new accounts.

Anyone looking for deposits at the moment? In fact I believe there’s a ‘war for deposits’ happening currently as the Fed raises rates. So don’t you want to make it as easy and accessible as possible for people to open accounts and GIVE YOU THEIR MONEY?

3. Crappy solutions (upgrading is not that much better than what we have)

Many of the solutions in the market today are, well, crappy. I recently reviewed an application experience at a credit union, delivered by a leading vendor in the DAO space, and the footer of the webpage said “© 2017” – it’s 6 years old!!! And that’s the new version of the experience. I listed 23 things that were wrong with the design and experience. So it’s no wonder people looking at this as an “upgrade” decide to do nothing. It’s not that much better.

But there are much better options in the market. Options that combine the 3 critical elements to make DAO successful:

- Exceptional customer experience

- Mitigate fraud

- Maximize funding

If you haven’t found a solution you’re impressed by yet, keep looking. They’re out there, I know.

4. Cost (My current solution costs $X, the new one is $5X)

Cost is probably the largest consideration for many institutions looking to upgrade their DAO offering or deploy a new one. The good solutions are more expensive than the crappy ones. But what amazes me about this is that the average institution is happy to invest $1.5M or so to establish a branch and $600k per annum to staff it. This is far more than any DAO solution I’ve seen in the market.

Plus, when you consider the fact that a successful DAO offering will outperform all branches combined AND reduce fraud AND deliver valuable deposits when there’s a war for deposits going on right now…then I think the case for investing is there.

Now the vendors can definitely do something to alleviate the pain associated with the cost of DAO solutions or put more skin in the game with transaction based pricing etc. But as an institution, if you work with the vendors in the market, I’m sure you’ll find a meaningful price point that delivers more value than you invest.

What can we do about it?

With over a decade working in digital account opening, I’ve formed some strong opinions on what works.

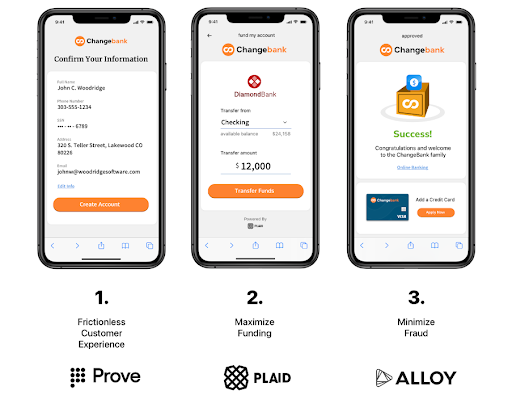

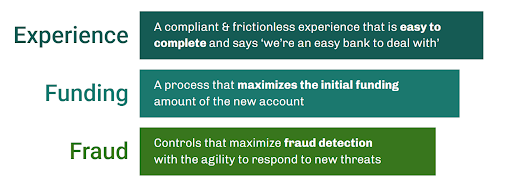

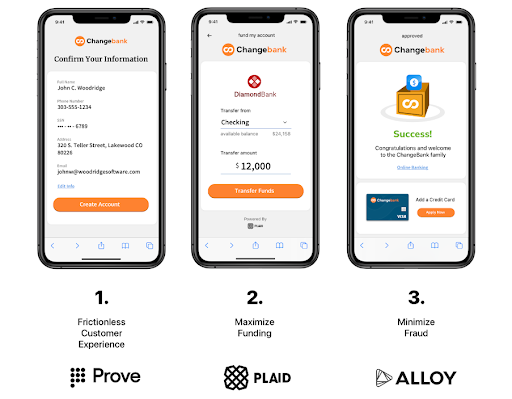

In my recent work with clients I’ve been encouraging them to continue to invest in DAO but to look for solutions and implementations that will deliver ALL of the following 3 elements – Experience, Funding and Fraud.

In a perfect world, we should have a DAO solution that “Delivers a frictionless customer Experience for account opening that maximizes the initial Funding amount for the account but at the same time minimizes the instances of Fraud in new account opening.”

Our recommendation is that the solution incorporates the following partners:

Prove – for prefilling from the applicant's mobile carrier. Not only is this a great customer experience, it is also a proven mechanism for minimizing fraud. When an applicant ‘types’ in their name, SSN, DOB etc – we have no idea if they’re the owner of that data or if they’ve bought it on the dark web. Ouch! But if we verify their device (with more than a one-time-password) and prefill data once verified – I have a much higher confidence level that you own that data.

Plaid – Plaid doesn’t just verify account ownership, it also returns the balance on the account we’re about to use to fund. What if we motivated the applicant to transfer more than the minimum funding amount? What if we offered a cash bonus or higher interest rate if they transferred more funds?

Alloy – With the constant evolution of fraud, we need a solution for fraud, KYC, AML, watchlists etc. that can respond as quickly as the fraudsters can innovate. Alloy is the best vendor we’ve seen in the market to do just that. We have one integration to Alloy, and then have hundreds of integrations to the leading data providers in the market. Experian, LexisNexis, Socure, FIS, etc. And we can easily turn services on/off based on the nature of the Alloy platform.

Conclusion

So let’s put an end to Ron Shevlin’s Groundhog Day. Let’s make 2023 the year that community banks and credit unions actually “FIX” their digital account opening and start reaping the benefits whilst there’s serious money to be made from deposits.